📊 The global shipping industry in 2026 is operating within a tight, supply-constrained environment, where asset values, charter rates, and capital deployment strategies are being redefined across offshore and tanker segments. In this market, pricing signals are no longer indicative while they are decisive.

📈 Real Market Pricing Signals – 2026

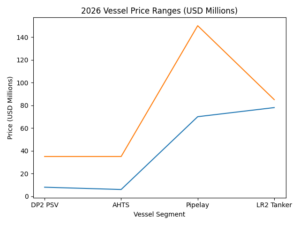

Offshore Support Vessels (PSV / MPSV / IMR)

- DP2 PSV (3,000 – 4,000 DWT | 2010 – 2015 built) : USD 8M – 20M (US units trading at premium up to +40%).

- Modern DP2 PSV (2016+ | high-spec / 1,000m² deck): USD 20M – 35M+

- Day Rates (North Sea / GoM) : USD 18,000 – 35,000/day (tightening upward).

👉 Signal: Strong upward momentum driven by offshore upstream recovery and vessel scarcity.

AHTS Vessels (DP2 / High Bollard Pull)

- 80T – 120T BP (2008 – 2015 built) : USD 6M – 14M

- High-spec DP2 AHTS (120T+ BP | 2016+ / newbuild resale) : USD 18M – 35M.

- Newbuild DP2 AHTS (60M – 75M LOA | 90T – 120T BP) : USD 12M – 28M (China / SE Asia yards).

- Day Rates (spot / project-based) : USD 25,000 – 60,000/day depending on region and scope.

👉 Signal: Tight supply, increasing subsea & drilling activity, strong forward demand.

Heavy-lift Offshore Assets (Pipelay / Construction Vessels)

- DP2/ DP3 Pipelay Vessels : USD 70M – 150M+ depending on specs and lay system.

- Day Rates (project basis) : USD 120,000 – 350,000+/day.

👉 Signal: Critical shortage globally – pricing firming aggressively due to limited fleet availability.

Tanker Market (LR2 / Aframax / Suezmax)

LR2 Tankers (Newbuild ECO / Scrubber) : USD 78M – 85M

Aframax (2015 – 2020 built) : USD 55M – 75M

Suezmax (modern units) : USD 65M – 90M

Time Charter Equivalent (TCE) :

LR2 : USD 28,000 – 45,000/day

Aframax : USD 30,000 – 50,000/day

👉 Signal: Supported by ton-mile expansion, sanctions-driven trade flows, and fleet inefficiencies.

Market Reality & Strategic Implications

These pricing signals confirm a structural shift in global shipping : –

- Second-hand asset values are firming or appreciating.

- Newbuild pricing remains elevated due to shipyard congestion (2026 – 2028 slots limited).

- Offshore vessels are transitioning from distressed assets to premium tonnage.

- Capital is returning aggressively into shipping via structured finance and leasing models.

Execution-Driven Shipowning in 2026

Shipowners must now operate as asset managers and capital allocators, not just operators.

Success depends on : –

- Entering assets before pricing peaks.

- Structuring deals with BBC, leasing, or hybrid financing.

- Maintaining fleet flexibility across offshore and tanker segments.

- Acting decisively in S&P transactions with qualified counterparties.

✅ Conclusion

The 2026 market is defined by pricing discipline, asset scarcity, and execution speed.

Those who understand and act on real pricing signals across PSV, AHTS, offshore construction, and tanker markets will dominate.

Those who hesitate will be priced out.