📊 All signals current as of this week. This is the most consequential convergence of shipbuilding demand catalysts in the United States since World War II.

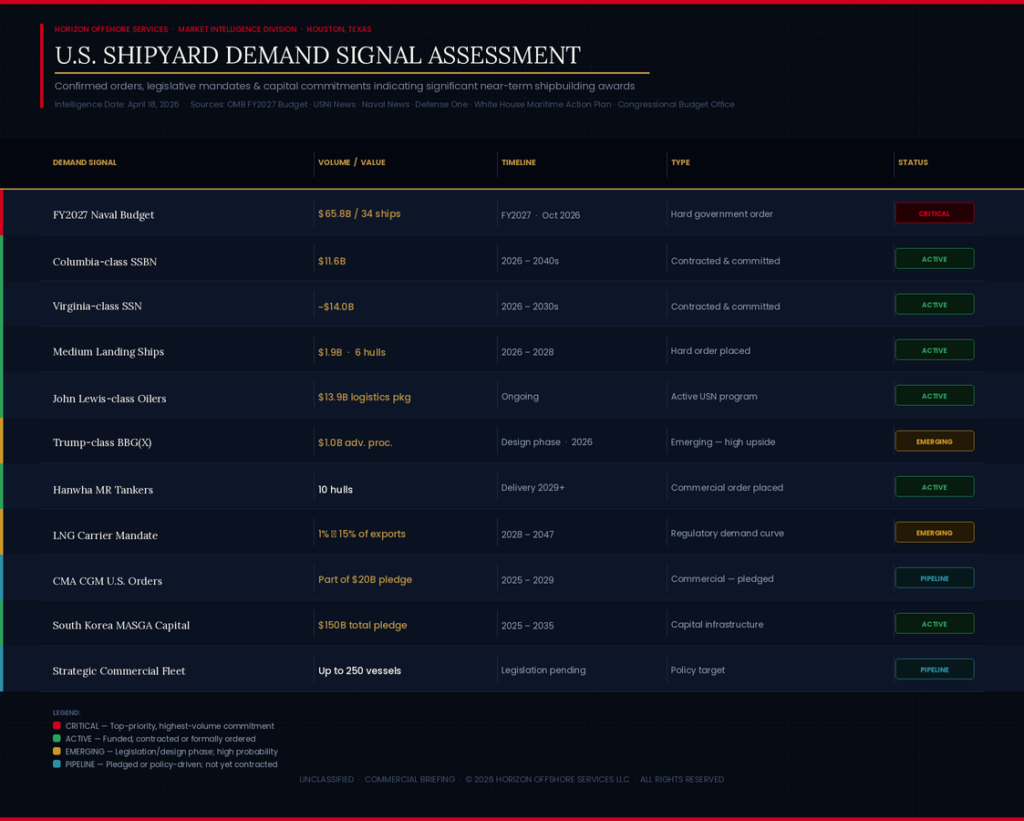

I. THE HEADLINE EVENT – FY2027 NAVAL BUDGET: US $65.8 BILLION / 34 SHIPS

On April 5, 2026, the Trump administration submitted its FY2027 budget requesting US $65.8 billion for naval shipbuilding – the largest request since 1962 – proposing 34 vessels including 18 battle force ships and 16 non-battle force ships. That represents a roughly 50% increase over the FY2026 enacted level of approximately US $42 billion.

The composition of that order is strategically important for commercial yards:

Submarines (highest priority, ~ US $25.6B combined): Columbia-class ballistic missile submarines receive $11.6 billion, while Virginia-class attack submarines receive nearly $14 billion, making it the single most expensive line item in the Navy’s request.

Surface combatants: One DDG-51 Arleigh Burke destroyer at US $3.27 billion, one FF(X) next-generation frigate at US $1.43 billion, and US $1 billion in advance procurement for the Trump-class BBG(X) battleship program.

Amphibious and logistics – the opening for commercial yards: Six Medium Landing Ships at US $1.89 billion, two submarine tenders, two John Lewis-class fleet oilers, one strategic sealift ship, one hospital ship, one T-AGOS surveillance ship, and one special mission ship. In a major departure, the U.S. is looking to existing commercial designs for many of these vessels – naval oilers will be built to commercial ABS classification rules, and strategic sealift vessels will be commercial ro-ros – a move that would allow more shipyards to get in the game at lower costs.

The “Golden Fleet” wildcard: Trump announced the concept of the USS Defiant (BBG-1) Trump-class guided missile battleship in December, stating the program would begin “immediately” with two ships, then quickly expand to 10, and eventually 20 – 25 vessels – the Navy’s first new battleship design since the Iowa class.

II. THE STRUCTURAL POLICY FRAMEWORK – EXECUTIVE MANDATES

The Trump administration’s America’s Maritime Action Plan, published February 13, 2026, calls for investing in upgrades to commercial shipyards including dry docks, cranes and utilities, forging public-private partnerships with tax incentives, and generating “predictable demand for U.S. built and U.S.-flagged vessels” through trade policy, customs enforcement, and federal acquisition reform.

The FY2027 budget also proposes formation of a new Maritime Security Trust Fund – designed to provide a mandatory and self-sustaining funding stream for shipbuilding capacity, fleet expansion, and workforce development – representing the most structurally significant financial mechanism proposed. Mondaq

Key MARAD allocations include US $500 million for port infrastructure, US $250 million for a new Commercial Shipbuilding Infrastructure Development Program targeting larger yards, and US $105 million for the Small Shipyard Grant Program – US $70 million above current levels. Holland & Knight

III. COMMERCIAL ORDER PIPELINE – SECTOR BY SECTOR

Jones Act Fleet Renewal: The Jones Act fleet has shrunk from 181 ships in 2000 to 93 ships today. Entire vessel categories are missing from the U.S.-built fleet including semisubmersible heavy transport vessels, dry-bulk ships, chemical tankers, LPG tankers, and LNG tankers. Each gap represents a direct order opportunity as policy mandates push domestic content requirements.

LNG Carriers – The White Space: The United States has not built an LNG tanker in more than four decades. From 2028 onwards, a new requirement mandates that 1% of exported LNG be carried by U.S. built, flagged, and operated vessels, increasing gradually to 15% by 2047. With the U.S. being the world’s largest LNG exporter, this creates a decades-long structural order book that does not yet exist.

Medium Range Tankers: Hanwha Shipping has ordered 10 MR oil and chemical tankers from Hanwha Philly Shipyard, the first due for delivery in 2029 – the first significant commercial tanker order placed at a U.S. yard in years.

Strategic Commercial Fleet: The SHIPS for America Act calls for a Strategic Commercial Fleet of up to 250 commercially viable, militarily useful, privately owned vessels – compared to the current U.S. oceangoing fleet of fewer than 200 vessels, of which only approximately 80 participate in international commerce.

CMA CGM Commitment: French shipping conglomerate CMA CGM committed to allocate $20 billion in U.S. shipping investments over four years, including container port infrastructure upgrades and placement of new orders in U.S. shipyards.

IV. FOREIGN CAPITAL POURING INTO U.S. YARDS

➡️ This is the most accelerated private capital inflow into U.S. shipbuilding in the modern era.

Hanwha Ocean / Philly Shipyard: South Korea committed US $150 billion in investment in U.S. shipbuilding as part of the U.S.-South Korea trade agreement, with Hanwha’s US $5 billion Philly Shipyard investment forming the flagship element – 50 times the US $100 million Hanwha paid to acquire the yard in December 2024. Hanwha plans to construct two new dry docks and three additional piers, aiming to increase annual production capacity from fewer than two vessels to 20 vessels per year, with ambitions to build LNG carriers, naval modules, and ultimately U.S. naval vessels including submarines.

HD Hyundai / HII Partnership: In April 2025, Huntington Ingalls Industries Newport News Shipbuilding signed an agreement with a South Korean shipbuilder to share best practices and collaborate on shipbuilding. HD Hyundai has signed an agreement with HII to jointly design and build the U.S. Navy’s next-generation logistics support ships.

Samsung Heavy Industries / Vigor Marine: Samsung Heavy Industries is partnering with Vigor Marine Group to provide expanded forward-deployed maintenance, repair and overhaul capacity to the U.S. Navy and Military Sealift Command across the Indo-Pacific

V. THE 30-YEAR NAVAL CONSTRUCTION CURVE

Over the past decade, the amount of naval tonnage under construction at U.S. shipyards increased 80%. Under the 2025 long-range plan, tonnage of submarines, surface combatants, and amphibious warfare ships under construction from 2030 to 2054 would be 50% higher on average than today. The CBO estimates the fleet reaching 390 ships by 2054.

The Heritage Foundation and Naval analysts are calling for a “Naval Act” block buy – locking in US $150.56 billion in ship purchases across 10 destroyers, 7 frigates, 10 attack submarines, 4 ballistic missile submarines, 3 amphibious transport docks, 1 amphibious assault ship, and 6 oilers – to give shipyards multi-year production certainty

VI. CAPACITY CONSTRAINTS – THE FRICTION LAYER

➡️ The demand signal is enormous. The constraint is real and must be priced into any commercial assessment:

U.S. shipyards accounted for less than 0.04% of global commercial output in 2024. A large commercial vessel built in the United States costs up to $250 million – roughly five times a comparable foreign-built vessel. Oil tankers priced at US $47 million internationally can exceed US $220 million in U.S. yards.

Currently fewer than 1% of new commercial ships are built in the United States. Of the country’s 66 shipyards, eight are fully new-build yards while 11 have some capacity to build new ships.

As of early 2026, submarine production is under sustained capacity strain, with about 25 strategic outsourcing arrangements in place to offload work from the two primary submarine construction yards.

HORIZON OFFSHORE SERVICES – BOTTOM LINE ASSESSMENT

➡️ 2026 is not a capital-constrained market – it is a capital-optimization market.

The United States is experiencing the most concentrated convergence of shipyard demand catalysts since 1945. The FY2027 budget alone – if Congress appropriates it – would inject more money into naval shipbuilding in a single year than the entire prior decade of average annual spending. The auxiliary and logistics vessel categories (oilers, ro-ros, hospital ships, submarine tenders) deliberately use commercial designs to open orders to yards beyond the six traditional naval primes. LNG carrier construction mandates create a guaranteed multi-decade order book. Foreign capital – particularly the $150 billion South Korean commitment with Hanwha as its anchor – is rebuilding physical capacity that atrophied for 40 years.

The constraint is execution capacity, skilled labor, and supply chain depth – not demand. For Horizon Offshore Services and Offshore Vessel Owners/ Operators, the implication is significant: U.S. yards will be at or near capacity for the next decade, lead times on Jones Act vessels will extend, and vessel valuations for existing compliant tonnage will strengthen materially.

For confidential financing, shipyard or marine assets acquisitions, contact management@horizonoffshoreservices.com